SECTION 5: CAPITAL STRUCTURE AND FINANCING

The Notes in this section describe the changes in the financial structure of Ferrovial as a result of variations in equity (see Note 5.1) and in its consolidated net debt (see Note 5.2), taken to be the balance of cash and cash equivalents net of the financial debt, bank borrowings and debt securities, making a distinction between non-infrastructure project companies and infrastructure projects. They also describe the Group’s exposure to the main financial risks and the policies for managing them (see Note 5.4), as well as the derivatives arranged in connection with those policies (see Note 5.5).

The equity attributable to the shareholders (see Note 5.1) decreased with respect to 2015, due to the impact of expense recognised directly in equity (arising from the exchange rate effect, pensions and derivatives) and to shareholder remuneration, which was offset in part by the increase in the consolidated net profit.

Equity attributable to the shareholders |

|

(Millions of euros) |

|

Beginning balance at 01/01/16 |

6,058 |

Net profit |

376 |

Income and expense recognised directly in equity |

-428 |

Transfers to profit or loss |

141 |

Shareholder remuneration |

-544 |

Other |

-7 |

Ending balance at 31/12/16 |

5,597 |

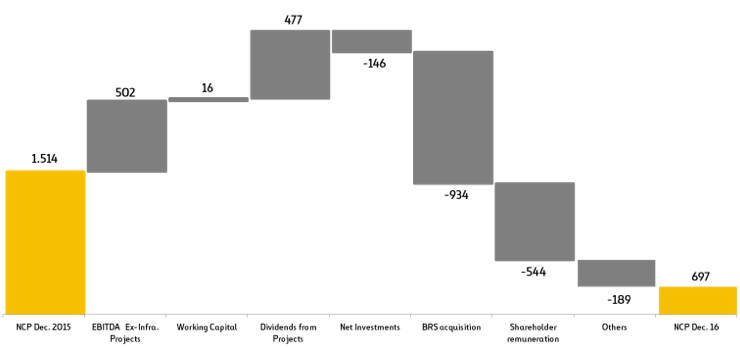

The consolidated net debt of Ferrovial’s non-infrastructure project companies is a positive net cash position of EUR 697 million, lower than it was at 31 December 2015 (EUR 1,514 million), mainly due to the effect of acquisition of Broadspectrum, with a total impact of EUR 934 million on the net cash position (EUR 499 million relating to the purchase price and EUR 435 million relating to the net cash position included on the acquisition date). The other changes are analysed through cash flows (see Note 5.3).

NET CASH POSITION NON-INFRASTRUCTURE PROJECT COMPANIES:

The consolidated net borrowings continue to make it possible to amply achieve the objective of maintaining an investment grade rating, where the Company considers a relevant metric a ratio, for non-infrastructure projects, of net debt (gross debt less cash) to gross profit from operations (EBITDA) plus dividends from projects of no more than 2:1. Ferrovial’s rating remains unchanged at BBB.

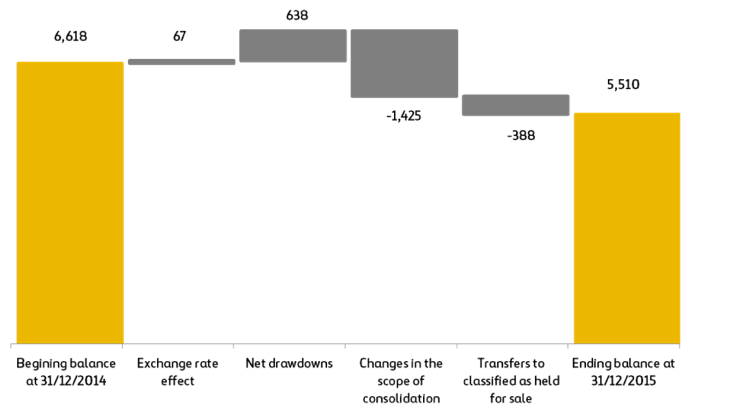

There was a drop in the gross borrowings of infrastructure projects, due largely to the exclusion from consolidation of the SH-130 toll road, as discussed in Note 1.3, and the reclassification of the liabilities of the Portuguese toll roads to "Liabilities Classified as Held for Sale".

BORROWINGS OF INFRASTRUCTURE PROJECTS: